En résumé

Le modèle économique dual d’Altarea entraîne des moteurs économiques distincts pour chaque segment.

Immobilier de détail

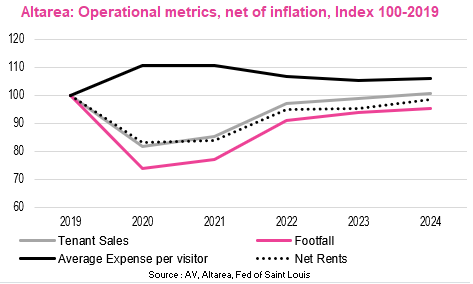

Altarea opère dans le format immobilier le plus résilient d’Europe : le commerce de détail. Cela implique la possession d’espaces commerciaux et leur location à des marques nationales ou internationales. Ces propriétés sont principalement “non-prime” à l’échelle mondiale mais ont une importance régionale ou continentale significative. Parmi les actifs notables figurent Cap 3000 à Nice, qui attire plus de 10 millions de visiteurs par an (et Qwartz, 8 millions), démontrant une résilience depuis la crise du COVID.

Au niveau de l’EBITDA, le flux de trésorerie est généré par la gestion des facteurs opérationnels tels que le taux de vacance, les ratios d’effort, les loyers nominaux, les coûts de gestion et d’entretien, les incitations, tout en tenant compte des contraintes environnementales comme le PIB, les unités de vente au détail concurrentes dans la zone de chalandise, l’accessibilité et la démographie. Suite à la récente période inflationniste, nous manquons d’informations sur le potentiel de réversion restant, qui est la différence entre les loyers en cours et les revenus potentiels en cas de relocation totale. Par conséquent, nous ne pouvons pas évaluer la croissance potentielle des loyers nominaux dans les années à venir, surtout nette d’inflation. Nous considérons donc que la génération actuelle de flux de trésorerie opérationnel est proche de l’optimal, en supposant un périmètre constant et net d’inflation, à partir de 2026, après les derniers effets favorables de l’indexation en 2025.

Les propriétaires actuels bénéficient actuellement et continueront de bénéficier d’une augmentation quasi nulle de l’espace de vente au détail concurrent en France. Cela se traduit par une offre maximale relativement fixe à la fois à l’échelle nationale et locale, créant un marché “sclérosé” qui favorise les propriétaires dans les zones à forte croissance démographique.

Altarea privilégie un taux d’occupation élevé pour ses actifs, même si cela nécessite une certaine flexibilité avec les loyers, afin de maintenir le trafic. Le taux d’occupation actuel est frictionnel, mais nous manquons de données détaillées pour une évaluation complète. Sur la base de notre expérience et de l’analyse des pairs d’Altarea, nous considérons que la gestion des actifs de détail d’Altarea est de haute qualité. L’entreprise fait preuve d’une gestion proactive et efficace sur site, illustrée par des politiques d’incitation réactives. Le taux de rotation de la base de location est nettement supérieur à la moyenne, ce qui indique une forte orientation commerciale.

Les informations sur les frais de gestion et la structure des coûts du segment de la gestion d’actifs pour compte de tiers sont limitées. Cependant, nous pensons que sa contribution à l’EBITDA récurrent (part du groupe) est relativement faible même si elle est très rentable (EBITDA/Capital employé). Cela s’applique également aux actifs en copropriété avec des actionnaires minoritaires mais gérés par Altarea. Notamment, des investisseurs tiers détiennent environ 57% des 5 milliards d’euros d’actifs sous gestion consolidés.

Développement résidentiel

La rentabilité du développement résidentiel dépend de la sécurisation des prix des terrains, des variations des coûts de construction et de la solvabilité des clients. Les marges opérationnelles ont dépassé 10% au début des années 2000 mais sont tombées à 6-7% entre 2018 et 2022. Le succès d’Altarea est dû à l’acquisition de terrains bon marché dans les années 1990, précédant le boom immobilier et les taux d’intérêt bas des années 2000. Le recyclage des liquidités et la prise de risques stratégiques ont façonné le profil actuel d’Altarea. À long terme, Altarea se concentre sur la gestion de la taille et du profil de risque, notamment par le biais de la dette, en fonction des conditions économiques et des attentes des actionnaires.

La marge opérationnelle du développement résidentiel n’est pas le seul indicateur ; le ratio EBIT/marge brute et le ROCE sont cruciaux. Alors que le capital engagé est généralement à faible risque, une destruction de valeur significative s’est produite entre 2022 et 2024, soulignant les risques cycliques. Les années de crise peuvent éroder un tiers à la moitié de la création de valeur accumulée.

Le contrôle des coûts et des risques est essentiel. En période de faible inflation, les prix du marché sont fixés par la solvabilité des clients, bénéficiant de la concurrence des sous-traitants. En fonction des facteurs macro, les marges peuvent être élevées ou modérées, comme on l’a vu depuis 2022. Nous prévoyons un retour à des marges positives de 3 à 5%, appliquées à des revenus potentiellement toujours faibles en 2025-27.

Gestion des coûts

Les coûts d’exploitation d’Altarea sont en grande partie variables et peu susceptibles de changer de manière significative. Le contrôle des revenus est plus critique que le contrôle des coûts, en particulier dans le segment de l’immobilier de détail.

Dans la phase actuelle du marché, Altarea peut accepter une sous-rentabilité opérationnelle pour maintenir son expertise, ce qui pourrait permettre un rebond rapide des marges si les conditions du marché s’améliorent.

Frais financiers

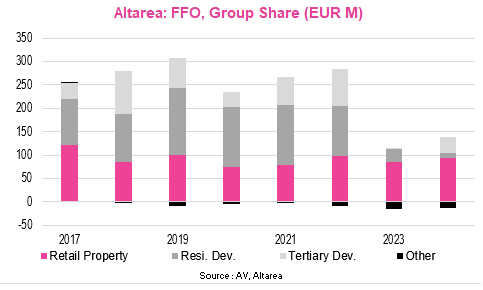

Le coût moyen de la dette d’Altarea est inférieur à 2% en 2024, appliqué à 2 milliards d’euros de dette nette en espèces, ce qui entraîne 34 millions d’euros de frais financiers récurrents en espèces. L’alignement sur un coût marginal de 5,2% augmenterait les dépenses de c.50 millions d’euros (part du groupe, estimation AV), par rapport à 127 millions d’euros de FFO en 2024.

Avec une couverture de la dette jusqu’en 2027, les changements à court terme sont peu probables, mais les impacts du roulement de la dette à moyen terme sur le FFO nécessitent une surveillance attentive. L’impact net sur le FFO dépendra de la reprise du FFO du segment Développement au niveau de l’EBITDA.

La direction d’Altarea est consciente de ce défi. Le risque persistant de frais financiers plus élevés pourrait entraver un retour rapide à 300 millions d’euros de FFO et affecter la dimension du niveau de dividende durable.