Pros

- Cementir is about white cement, a niche that offers growth and better margins as a higher value-added product. It controls 20% of the addressable market

- It has an excellent record at pivoting assets and making those sweat with Denmark, the US and Belgium as the current hubs

- Cementir Holding is well exposed to the Turkish market, which is set to supply cement for Ukraine and Syria's reconstruction due to significant overcapacity

Cons

- Absolute market size is capped in white cement meaning that Cementir relies on its Belgian and Danish assets to grow local grey cement franchises

- As a family business, it leaves no room for third-party openings and suffers from a limited float

- Currency devaluations in Turkey and Egypt remain a key concern, as they significantly weigh on the company's results despite the positive volume trends in both markets

| | |

|

12/24A

|

12/25A

|

12/26E

|

12/27E

|

12/28E

|

|

PER ajusté (x)

| | |

7,63

|

10,7

|

13,3

|

12,3

|

11,7

|

|

Rendement net (%)

| | |

2,83

|

2,10

|

2,12

|

2,12

|

2,12

|

|

VE/EBITDA(R) (x)

| | |

3,23

|

4,02

|

4,01

|

3,50

|

3,09

|

|

BPA ajusté (€)

| | |

1,30

|

1,33

|

1,07

|

1,15

|

1,21

|

|

Croissance des BPA (%)

| | |

0,00

|

2,52

|

-19,7

|

7,39

|

5,12

|

|

Dividende net (€)

| | |

0,28

|

0,30

|

0,30

|

0,30

|

0,30

|

|

Chiffre d'affaires (M€)

| | |

1 687

|

1 640

|

1 734

|

1 836

|

1 945

|

|

Marge d'EBITDA/R (%)

| | |

24,1

|

28,1

|

23,6

|

23,8

|

23,8

|

|

Résultat net pdg (M€)

| | |

202

|

206

|

166

|

178

|

188

|

|

ROE (après impôts) (%)

| | |

12,5

|

11,6

|

8,76

|

8,89

|

8,81

|

|

Taux d'endettement (%)

| | |

-14,8

|

-20,4

|

-27,1

|

-31,1

|

-34,4

|

|

Next Div. Indic 0,28 € payment 19/05/2027

|

|

Potentiel

67,5 %

Cours (€)

14,16

Capi (M€)

2 253

|

|

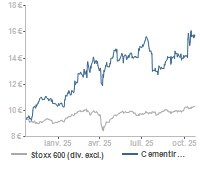

Perf. 1S:

|

-4,90 %

|

|

Perf. 1M:

|

-4,97 %

|

|

Perf. 3M:

|

-7,09 %

|

|

Perf Ytd:

|

-23,0 %

|

|

Perf. relative/stoxx600 10j:

|

-0,31 %

|

|

Perf. relative/stoxx600 20j:

|

-5,84 %

|

|