Introduction

Cementir, a global cement player with Italian roots, is the kingpin in white cement (with a 20% market share excluding “off”-white cement). Denmark is by far its biggest market (30% of revenues in 2018). The company strives to develop strong local market share in grey cement and a noteworthy global market share in white cement.

Like its French peer Vicat, Cementir is a family-driven business that has maintained a solid balance sheet throughout its volatile industrial cycle, with its net debt/EBITDA consistently below 3x. It stands unique as it dodged costly acquisitions during the top of the cycle (2007-08) and, ergo, avoided the need for fresh-but-dilutive capital at the bottom of the cycle (2008-09).

Cementir believes in fair-priced acquisitions which have strategical location and well maintained assets. Its past deals helped it to develop a white cement franchise with strong and recurrent cash flows (mainly linked to the renovation market) which could be the cash cow to a careful expansion in the bigger but more cyclical grey cement market. Yet, with the current focus on sustainability and digitalisation, we evaluate the likelihood of its inorganic growth as low.

Operations

Cementir has operations in 18 countries across five continents. In addition to white cement, it is involved in grey cement, ready mix, aggregates and the processing of urban and industrial waste.

What makes Cementir unusual is its exposure to the underpenetrated and more lucrative white cement business (20% global market share, excluding “off-white” and lower quality Asian products). White cement provides a great white space opportunity as it trades at twice the price of grey cement (local comparison) and accounts for about 1% of grey cement volumes. Given its higher unit value in comparison to white cement, it can be more easily transported, opening the company’s gates to global markets. This has in turn made Cementir the leader of traded flow, with export sales representing about 25% of total exported volumes globally. Furthermore, its local presence with a sales force and/or controlled logistic networks in about 20 key target markets enhances its exports. The group aims to export 50% of the white cement produced by 2020, which is an ambitious but achievable target in our opinion.

White cement relies on scarce yet extra-pure limestone, accompanied with sand, gypsum and alu silicates. These hardly exist in certain countries such as Brazil, Australia and parts of Africa. The chemical composition of the limestone used in white cement is such that the burning process requires a higher temperature and eats up roughly 50% more energy as compared to grey cement.

Waste management as part of the cement value chain

For a decade, Cementir has been strategically including waste management in its value chain. In 2009, Cementir entered the Turkish waste management business through the acquisition of Sureko AS and reinforced its presence through the acquisition of Recydia in 2011 (waste management and renewables business). It was then complemented by the acquisition of NWM Holdings (UK) which collects, treats, recycles and disposes of waste. Since Cementir has no cement plants in the UK, we believe that the goal is to use this waste as fuel in the Denmark kilns to reduce energy consumption (as waste has higher calorific value than traditional fuels) and leave a greener footprint because the wastes would have been incinerated otherwise as well. Cementir’s waste business’s standalone profitability might seem low but it enables the group to address environmental issues significantly.

Contrarian strategy?

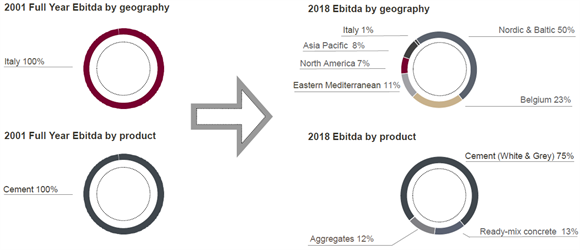

Cementir has grown from a medium-sized Italian “single-country” and “single-product” operator into a fully-fledged multinational company, without any increase in share capital, thanks to surplus operating cash flow generation.

In 2001, the Cementir Group embarked on its geographic diversification process, by acquiring Cimentas in Turkey. This was followed by a product diversification through the acquisition of Aalborg Portland in 2004, a white cement manufacturer.

However, the most radical transformation of the Cementir Group portfolio came between 2016 and 2018. It acquired the cement and concrete business of Sacci SpA (2016), expanded its international presence by acquiring CCB (2016), sold off all Italian assets in 2018 (with only the central headquarter and some trading businesses remaining in Italy) and, lastly, acquired a majority shareholding in Lehigh White Cement Company (LWCC) in the US (2018) – making Cementir a leader in this promising niche market with a market share of ~20%.

Two decades of work results in the exit of Italy and a well-diversified portfolio

Products’ analysis

The Cement division (€700m of sales)

Cementir produces about 10mt of grey and white cement via Aalborg Portland, the leader in Denmark, and Lehigh White Cement Company in the US, while its Chinese, Egyptian and Malaysian subsidiaries are the leading producers of white cement in their respective domestic markets.

In 2018, Cementir produced 7.3mt of grey cement mainly from the six plants in Denmark, Belgium and Turkey and 2.5mt of white cement. Cementir is the world’s leading producer and exporter of white cement, which is a well-profitable business as sales are generally B2B where switching costs are high.

Ready-mixed concrete (4.9mm3 sold, €429m of sales)

Ready-mixed concrete is widely used in construction activities. The group owns 105 concrete mixing plants (37 in Denmark, 28 in Norway, 9 in Sweden, 16 in Turkey, 10 in Belgium, 5 in France) with a strong hold in Denmark and Norway.

Aggregates (10mt sold, €87m in sales)

Aggregates is a small yet profitable (EBITDA margin at 32%) business. The group owns 11 quarries (3 in Belgium, 5 in Sweden, and 3 in Denmark).

Waste (€108m in sales)

Waste is being successfully used as an alternative fuel. Cementir was one of the first industrial players to capitalise on this since 2009. Cementir Group’s treatment plants produced a total of 100,000 tons of fuel from waste in 2018, or c. 20% of its fossil fuel needs in 2018.

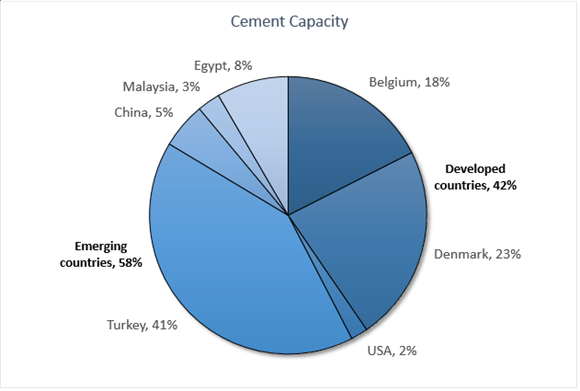

Cement capacity split and utilisation rate

41% of the group cement capacity is located in Turkey, which has been a drag over the past few quarters.

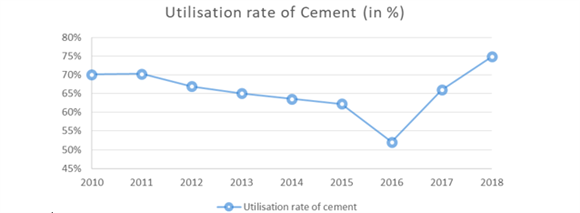

At 75% in 2018, the utilisation rate was at its highest for a decade. Compared to other cement companies in the AlphaValue universe, it outperforms LafargeHolcim, HeidelbergCement and Buzzi (~70%) and is at par with Vicat (~75%).

Geographical diversification

Cementir enters the Belgian market…

In 2016, Cementir acquired Compagnie des Ciments Belges (CCB) in a competitive bidding process for €312m on a cash and debt-free basis. This included an integrated plant with a capacity of 2.3 million tons, 3 aggregates quarries (one of which is the biggest quarry in Europe) and 10 ready-mix plants. The cement plant located in Gaurain is the largest in France-Benelux, with a state-of-the-art technology, well-developed logistics and mineral reserves with long life (over 80 years).

This deal helped address the core of Western Europe, with a low risk profile but at the detriment of lower growth prospects than in emerging markets.

...exits Italy…

In Q1 18, Cementir sold all its operations in Italy to HeidelbergCement for €315m on a cash and debt free basis. This included 5 fully integrated plants, 2 grinding centres, 6 terminals and several ready-mix plants. The disposal of the loss-making Italian activities brought the group debt/EBITDA to about 1x and opened fresh consolidation options.

...and reinforces its presence in the US

In Q1 18, Cementir reinforced its position as a global leader in white cement by acquiring an additional 38.75% stake in Lehigh White Cement Company (LWCC) (to reach 63.25%), which is the leading supplier and distributor of white cement in the US. The local white cement capacity is low at only 0.26m tons, but this is backboned by high imports from the plants operated by Cementir in other countries (Egypt, Denmark notably) and from the plants operated by Cemex, which owns the remaining 36.75% stake in LWCC. Extensive inbound and inland logistics are the key competitive advantages for Cementir in the US. As the company targets to export 50% of its white cement production, the LWCC deal was key in order to get an exposure to this import-led market.

The group aims to gain market share in the US and hence it may not hike prices for a year or two. We concur with this strategy because Cementir’s main goal is to achieve a 50% exports target, and importing from Denmark and Egypt to meet the market demands will not only increase the market share in the US but will help with meeting the export targets as well. Hence, the LWCC deal was essential for this strategy.

China: the most profitable market going forward?

China, along with Malaysia have so far been the most profitable and highest growth markets for Cementir (sales CAGR = 4.7% and average EBITDA margin = 23% over 2013-18). Sales in China are mostly local and focused on premium white cement, unlike the other Chinese players which provide lower grade “off”-white cement.

In 2016, the Chinese Ministry of Industry and Information Technology published guidelines on eliminating outdated production capacity in cement, which may phase out at least 500mt of ‘low-grade’ grey cement production capacity. On top of this, an unprecedented consolidation may take place in China’s cement industry by 2020. These may impact the white cement market as high-quality assets are mostly owned by big players. The aforementioned reasons support our investment thesis that China could be the most profitable market for cement in future.

Egypt: a sharp rebound potential

In Egypt, Cementir operates mainly in the Sinai Peninsula, where the operations were dragged down by security concerns in 2018. Devaluation in FX, temporary shutdown of the plants and barriers in transportation caused a decline in sales volume and prices. However, the Q1 19 results showed a recovery with a doubling in sales. Also, the competitive picture has been embellished as there are now only two players left in white cement. However, we believe that this is insignificant as a major part of the production is exported to other countries such as the US.

Outlook for grey cement

Cementir is the only Danish producer of grey cement with a significant market share, despite imports from the Baltic States and Northern Germany. It is a steady market in which the demand for cement is expected to grow by about 2% over the long term. Exports are focused on mainly Norway and Iceland. Denmark represents 21% of the group’s grey cement capacity as well as 40% of EBITDA, with a cash conversion ratio as high as 75%.

After the acquisition of CCB in 2016. Belgium accounts for a sizeable portion of both capacity (19%) and EBITDA (23%). Sales in Belgium are driven by: i) a residential market supported by renovation and infrastructure, and ii) large exposure to France, the Netherlands and Germany. France pulls with its infrastructure and concessions spending, with the Summer Olympics 2024, as well as with the Grand Paris underground.

In the past, Turkey has posted one of the highest levels of per capita grey cement consumption. However, the devaluation of the lira and rapid inflation, accompanied by political tension from 2018 onwards, has caused the GDP growth in 2019 to plummet (from 7.4% in 2017 to 1% in 2019). Volume improvements are bound to be slow. The best of the Erdogan years is probably behind but the group holds a long-term positive view which can be clearly seen by the green investment in the Izmir plant.

Market size and industry analysis

Expected growth higher for white cement

There is an ongoing commercial push to “create and grow the market” for white cement while the market for grey cement is pulled by demand. White cement demand is set to increase by an average of 1.8% p.a. between 2018 and 2023, expanding from 17.5mt to 19.4mt. From a regional perspective, China and Asia ex-China, are expected to lead growth in white cement consumption.

White cement is a more rewarding premium business. While grey cement is a standardised €200bn market with around 2bnt of production per year excluding China, white cement is a €4bn niche market with only about 20mt of production per year.

Growth of the white cement market is expected over the medium term to be higher than grey cement because:

- there is a cannibalisation effect of grey cement by white cement due to the added functionalities/applications it offers;

- cement usually represents less than 5% of total construction costs and white cement is only twice the price of grey cement, thus demand is inelastic to prices;

- white cement can replace grey cement in practically every application;

- there are virtually unlimited applications for white cement: pre-stressed concrete façade, paving blocks, artificial stone, Glass-Fibre Reinforced Concrete (GRC) façade, Ultra-High Performance Concrete (UHPC), dry mix mortars and Ready Mix Concrete (RMC);

- a defining feature of white cement is the possibility of producing coloured ready-mix or dry admixtures by mixing it with pigments.

INDUSTRY TRENDS

Alternative fuels

In order to decrease the environmental impact of the industry, improve the competitiveness of cement companies, and provide a viable and convenient end-of-life option for waste and industrial by-products, the use of alternative fuels is evolving.

CO2 taxation

After a decade of single-digit prices, European carbon now trades close to €30/t. The Emissions Trading System is at the root of the EU climate strategy. As part of its transition to a low-carbon economy, the EU targets to become carbon neutral by 2050 (compared to 1990 levels), in order to keep climate change below 2°C. Phase 4 of ETS (2021-30) will further reduce the allowances available (annual rate of decline from 1.74% currently to 2.2% (2021)).

Contrary to the power sector, the cement industry, which contributes 8% to the world’s CO2 emissions, receives net excessive free allocations from the EU ETS due to low production levels after 2008. This hardly led to any net reduction in GHG but a decline in the threshold accompanied with increasing carbon prices will incentivise manufacturers to put efforts in long-term solutions rather than relying just on the trading system.

Hence, keeping the lid on CO2 is essential to survive. Note that Cementir has free CO2 allowances up until the end of 2021, which is already a competitive advantage compared to some of the other cement companies.

Cementir’s actions

Some actions implemented by Cementir are as follows:

- A heat-recovery system has been built in Aalborg (Denmark). Most of excess heat is recovered and supplied to the Aalborg City district heating (36,000 households which may increase to 50,000 households by 2023). We believe that this heat recovery system is a way of maintaining a good relationship with the politicians and locals (i.e. external shareholders) of a green country like Denmark.

- About 400mt of industrial and urban waste are collected and processed annually in the group’s plants, as a way to reduce annual energy consumption. 40% of the total energy requirement in the Gaurain plant in Belgium is fulfilled by waste fuel and the group aims to increase this to 80% by 2023.

Megatrends

Urbanisation

The number of people living in cities increases by 50 million every year, and this figure continues to grow. By 2050, an estimated six billion people — or two-thirds of the world’s population — will live in cities. This growth in urbanisation will drive the demand for durable yet affordable workplaces and homes, which will in turn increase the demand for cement.

Global warming

With the increase in global temperature, the demand for sustainable yet affordable materials is increasing. Since roughly 8% of world’s CO2 emissions stems from the cement industry, cutting down this emission is a prerequisite. However, in booming economies from Asia to Eastern Europe, cement is literally the glue of the process, which makes it difficult to replace. Any resolute reduction in carbon emissions will have significant consequences for the construction materials industry.