Pros

- Cementir remains a global leader in white cement, a niche segment with resilient demand, especially in architectural and infrastructure applications. It controls around 20% of the market, offering stable margins

- A strong track record on asset optimisation with key profit centres in Denmark (white cement), the US, Turkey (grey cement and largest in volume) and Belgium

- The family-controlled company maintains financial discipline and a long-term industrial vision, including on greening up capex

Cons

- The white cement market is limited in size, making growth dependent on successful expansion or efficiency gains in grey cement operations, notably in Denmark and Belgium

- The family-controlled structure limits the free float and strategic flexibility, reducing the stock’s appeal for some institutional investors

- Turkey, one of the key production and demand markets for Cementir, brings with it geopolitical opportunities and thus risks

Synthèse

Prochaine publication : 29/07/2025

Prochaine publication : 29/07/2025

| | |

|

12/23A

|

12/24A

|

12/25E

|

12/26E

|

12/27E

|

|

PER ajusté (x)

| | |

6,04

|

7,63

|

11,7

|

10,8

|

10,8

|

|

Rendement net (%)

| | |

3,57

|

2,83

|

1,82

|

1,82

|

1,82

|

|

VE/EBITDA(R) (x)

| | |

2,69

|

3,23

|

5,03

|

4,52

|

3,99

|

|

BPA ajusté (€)

| | |

1,30

|

1,30

|

1,32

|

1,42

|

1,42

|

|

Croissance des BPA (%)

| | |

21,6

|

0,00

|

1,85

|

7,81

|

-0,27

|

|

Dividende net (€)

| | |

0,28

|

0,28

|

0,28

|

0,28

|

0,28

|

|

Chiffre d'affaires (M€)

| | |

1 694

|

1 687

|

1 749

|

1 840

|

1 985

|

|

Marge d'EBITDA/R (%)

| | |

24,3

|

24,1

|

23,7

|

23,4

|

22,7

|

|

Résultat net pdg (M€)

| | |

202

|

202

|

205

|

222

|

221

|

|

ROE (après impôts) (%)

| | |

14,0

|

12,5

|

11,5

|

11,5

|

10,5

|

|

Taux d'endettement (%)

| | |

-10,4

|

-14,8

|

-18,9

|

-23,4

|

-28,0

|

|

Next Div. Indic 0,28 € payment 19/05/2026

|

|

Potentiel

38,0 %

Cours (€)

15,4

Capi (M€)

2 450

|

|

Perf. 1S:

|

1,18 %

|

|

Perf. 1M:

|

10,0 %

|

|

Perf. 3M:

|

14,5 %

|

|

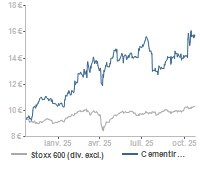

Perf Ytd:

|

49,0 %

|

|

Perf. relative/stoxx600 10j:

|

2,88 %

|

|

Perf. relative/stoxx600 20j:

|

8,90 %

|

|